Car insurance can be confusing, especially with all the different types of coverage available. One of the most commonly misunderstood types is collision insurance. Many drivers wonder: What exactly does collision auto insurance cover, and do you really need it? At Get Drivers Ed, we believe that understanding your insurance options is an essential part of being a responsible driver. In this blog, we’ll break down what collision auto insurance is, what it covers, how it differs from other types of car insurance, and whether it’s right for you.

1. What Is Collision Auto Insurance?

Collision auto insurance is a type of car insurance that specifically covers the cost of repairing or replacing your vehicle if it's damaged in a collision with another vehicle or object. Unlike liability insurance—which only covers damage to other people’s property or medical expenses if you’re at fault in an accident—collision insurance is all about protecting your own vehicle. This means that if you’re involved in an accident and your car sustains damage, your collision coverage can help cover the repair costs, regardless of who was at fault.

Key Points:

Collision insurance covers damage to your car from collisions with other vehicles or objects.

It helps pay for repair or replacement costs, reducing out-of-pocket expenses.

Collision coverage applies even if you are at fault in the accident.

2. What Does Collision Insurance Cover?

Collision insurance is designed to cover physical damage to your car resulting from specific types of incidents. Here are some of the main situations that collision insurance typically covers:

a. Collisions with Another Vehicle

If you’re in an accident with another car—whether you rear-end someone, get sideswiped, or are involved in a head-on collision—collision insurance will help pay for the damage to your car. This can be especially valuable if the accident was your fault, as liability insurance wouldn’t cover your own repair costs.

b. Collisions with Objects

Collision insurance also covers damage to your car if you hit an object, such as a tree, guardrail, fence, or pole. Even a single-vehicle accident, like losing control and crashing into a ditch, is typically covered under collision insurance.

c. Single-Car Accidents

Not all accidents involve other vehicles. If you roll your car or hit an obstacle on the road, collision insurance can still provide coverage. This is especially useful for drivers who frequently travel on rural or winding roads where single-car accidents are more common.

At Get Drivers Ed, we emphasize the importance of understanding the specific scenarios that your car insurance covers. Knowing what to expect in different situations can help you make informed decisions and avoid unexpected expenses.

3. What Collision Insurance Doesn’t Cover

While collision insurance covers a variety of incidents, it’s important to understand its limitations. Collision insurance is focused on accidents, but it does not cover everything. Here’s what collision insurance typically doesn’t cover:

a. Damage from Natural Disasters, Theft, or Vandalism

Collision insurance doesn’t cover damage resulting from events like hailstorms, flooding, theft, or vandalism. For these types of incidents, you would need comprehensive insurance. Comprehensive coverage is designed to protect your car from non-collision-related damage.

b. Medical Bills for Injuries

Collision insurance only covers damage to your vehicle, not any injuries sustained in the accident. For medical expenses, you would need personal injury protection (PIP) or medical payments coverage.

c. Damage to Another Person’s Vehicle

If you’re at fault in an accident, collision insurance won’t cover damage to the other person’s vehicle. This is where liability insurance comes into play. Liability insurance is required by law in most states, including Texas, and is designed to cover damages you cause to other people’s property or injuries in an accident.

At Get Drivers Ed, we help new drivers understand the different types of car insurance and why each type is important. Our online driver’s course covers essential information about auto insurance and responsible driving.

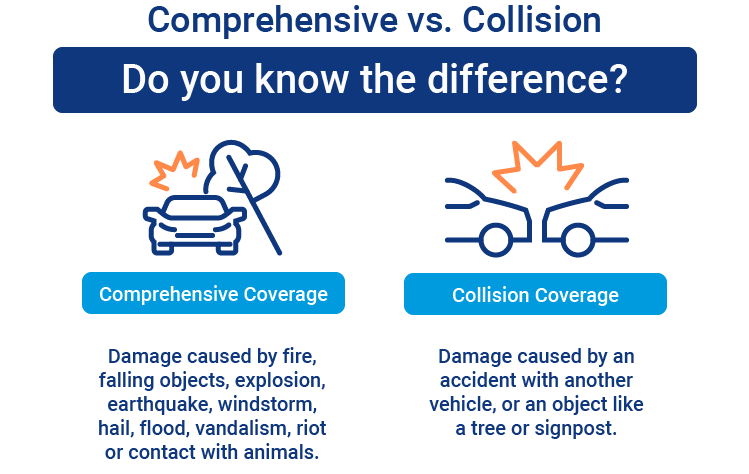

4. How Collision Insurance Differs from Comprehensive Insurance

Many people confuse collision and comprehensive insurance, but they cover very different things. While both are types of physical damage coverage for your car, they apply in different situations:

Collision Insurance: Covers damage resulting from collisions with other vehicles or objects, regardless of fault.

Comprehensive Insurance: Covers damage from non-collision-related incidents, such as natural disasters, theft, or vandalism.

A common recommendation is to have both collision and comprehensive insurance if you want full protection for your vehicle. This combination is often referred to as “full coverage.” However, it’s ultimately up to each driver to decide which types of coverage make sense for their situation and budget.

5. Do You Need Collision Insurance?

Collision insurance isn’t legally required, but it’s often a wise choice, especially for certain types of vehicles and drivers. Here are a few factors to consider when deciding whether collision insurance is right for you:

a. The Value of Your Car

If you have a newer or more expensive car, collision insurance can help you avoid paying high repair or replacement costs out of pocket. However, if your car is older and worth less, you may decide that collision coverage isn’t worth the premium.

b. Your Risk Level

Consider your driving habits and the area where you live. If you frequently drive in high-traffic areas like Austin, Texas, where accidents are more likely, collision insurance can provide valuable protection. At Get Drivers Ed, we know that urban driving comes with its own risks, and having collision coverage can bring peace of mind.

c. Leasing or Financing a Car

If you’re leasing or financing your vehicle, the lender may require you to have collision insurance. This is to protect their investment in case of an accident.

d. Financial Preparedness

Think about your financial ability to cover repairs if you were to get into an accident. Collision insurance can save you from a significant expense that could disrupt your finances.

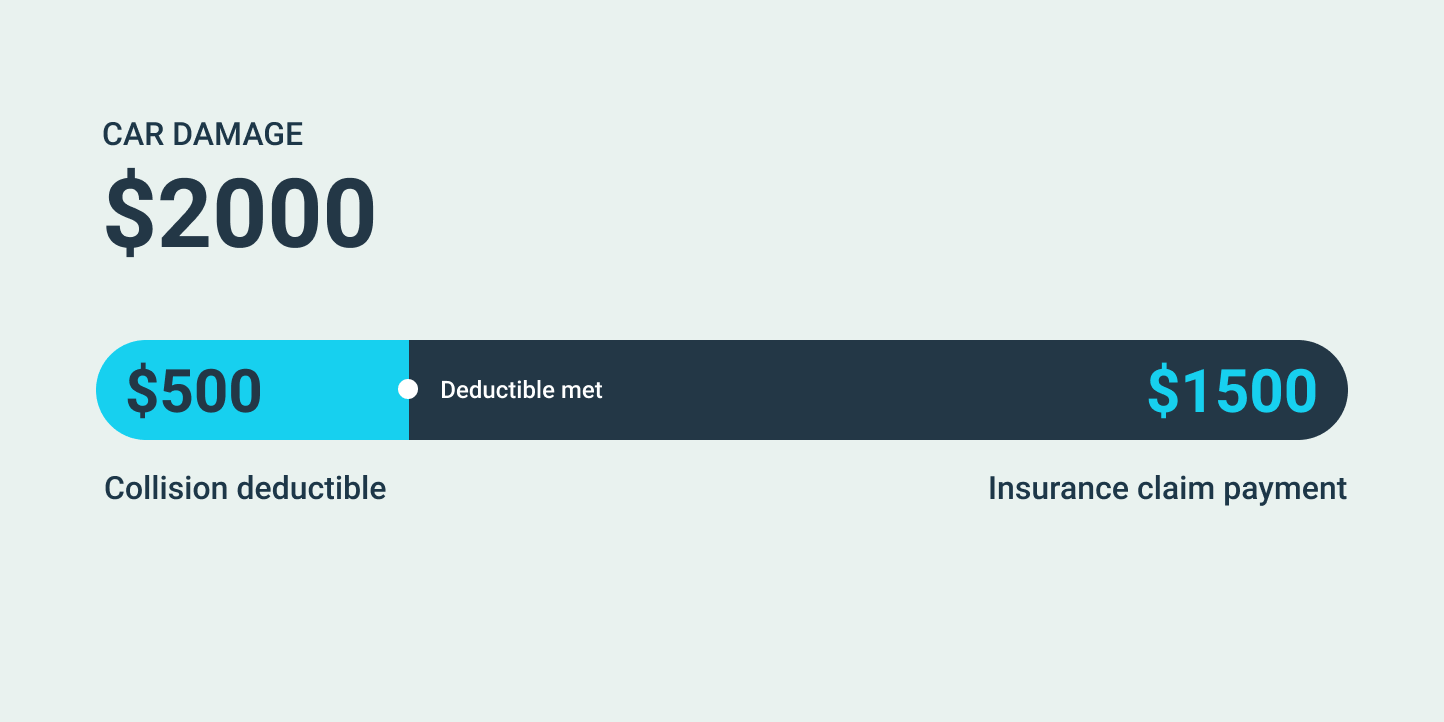

6. How Collision Insurance Works: Deductibles and Premiums

When you purchase collision insurance, you’ll typically choose a deductible, which is the amount you pay out of pocket before your insurance kicks in. Deductibles generally range from $250 to $1,000. Choosing a higher deductible can lower your premium, but it also means you’ll pay more in the event of a claim.

Example of How It Works: Let’s say you have a $500 deductible on your collision insurance. If you’re involved in an accident and the repair costs are $2,500, you would pay the $500 deductible, and your insurance would cover the remaining $2,000.

Balancing your deductible and premium is an important part of choosing the right coverage. At Get Drivers Ed, we encourage drivers to consider their budget and driving habits when selecting their insurance options.

Final Thoughts and Call to Action

Collision auto insurance is an important coverage option for protecting your vehicle from accident-related damage, whether it’s a collision with another car, an object, or a single-car accident. While it’s not legally required, having collision insurance can provide peace of mind and financial protection, especially for newer or high-value vehicles.

If you want to learn more about insurance and safe driving practices, consider enrolling in our online driver’s course at Get Drivers Ed. We’re dedicated to helping drivers understand the essentials of responsible driving, from road rules to insurance options, so you can feel confident and prepared behind the wheel. Don’t wait—start building your driving knowledge with Get Drivers Ed today!